How to Write a Freelance Invoice (With Examples)

A practical, jargon-free guide to writing a freelance invoice that gets paid on time. Includes the eight essentials, a worked example, and EU-specific notes on VAT and reverse charge.

Most late payments don't start with a difficult client. They start with a sloppy invoice. The wrong total. A missing reference. A bank account that doesn't match the one on file. Each small ambiguity becomes a reason for the accounts payable team to push the invoice to the back of the queue.

A clear, complete invoice removes those reasons. This guide walks through the eight essentials, a worked example, and the EU-specific bits you can't skip if you bill across borders.

The eight things every freelance invoice needs

These aren't style preferences — most jurisdictions legally require some combination of them, and any AP team will reject an invoice missing one. For the complete field-by-field list, including the EU-specific extras, see what to put on an invoice.

- The word “Invoice” at the top. Not “Statement,” not “Bill,” not “Payment Request.” The literal word triggers correct handling in most accounting systems.

- A unique invoice number. Sequential is fine (

INV-001,INV-002) but you can prefix with the year or client code if you bill many clients. The only rule: never reuse a number. - Issue date and due date. Both, explicitly. “Net 14” alone is ambiguous — write the actual due date.

- Your business details. Legal name, address, registration number if you're a registered entity, and a tax/VAT number if applicable.

- Your client's billing details. Their legal name (not the trading name), billing address, and tax ID if they're VAT-registered.

- Itemized line items. Each with a description, quantity, unit (hour, day, item), and rate. Don't lump multiple things into one line — AP teams will ask for the breakdown anyway.

- Subtotal, tax, total. All three, in that order, so the math is auditable. Show the tax rate and the tax amount separately.

- Payment instructions. Bank name, IBAN, SWIFT/BIC, and the account holder name. For non-EU clients, include the SWIFT — IBAN alone isn't enough.

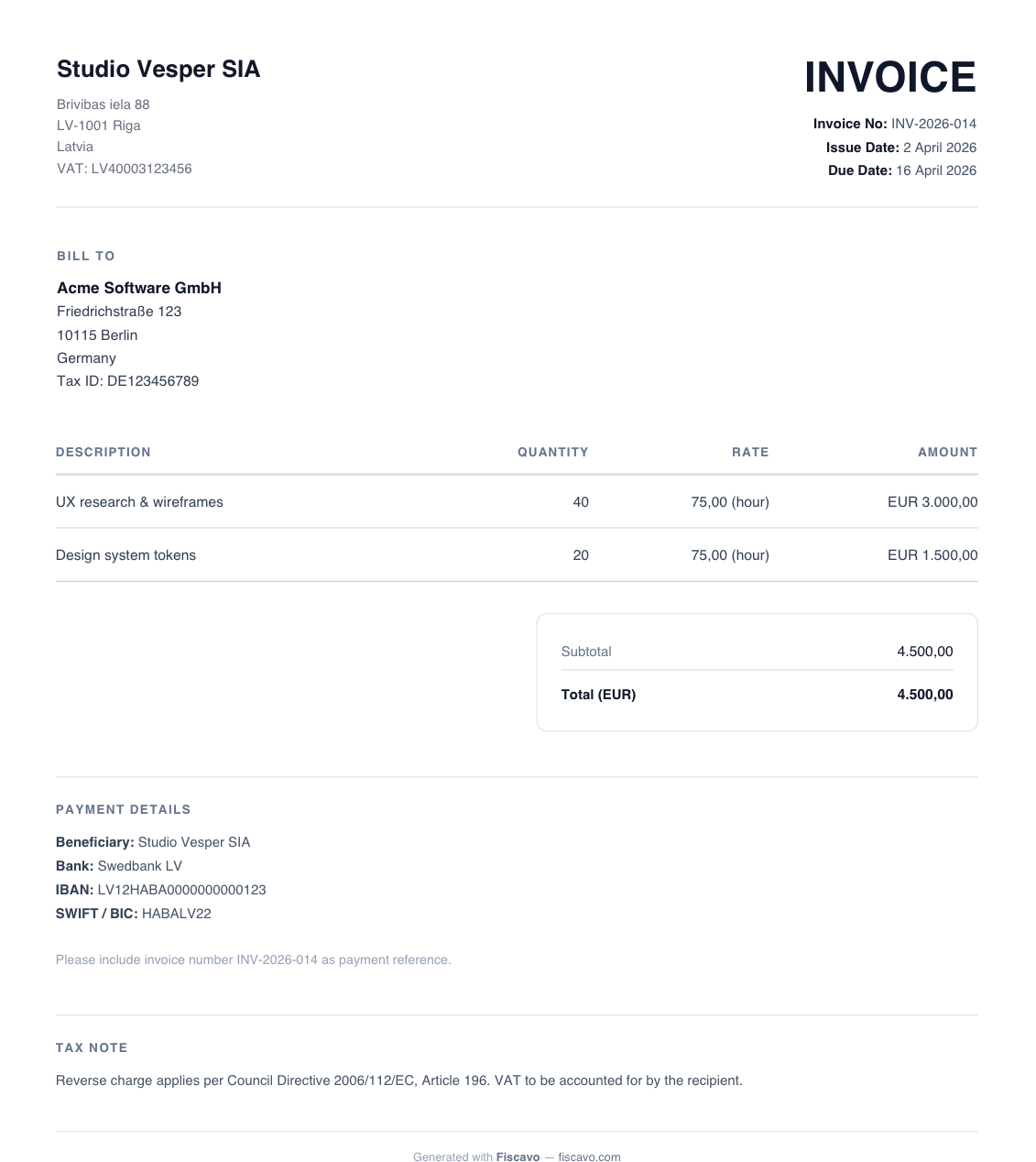

A worked example

Imagine you're a freelance UX designer based in Riga, billing a German client for two weeks of work. Here's what the invoice should look like:

- Invoice №

INV-2026-014 - Issued: 2 April 2026 · Due: 16 April 2026

- From: Studio Vesper SIA · Brīvības iela 88, Riga LV-1001 · VAT LV40003123456

- Bill to: Acme Software GmbH · Friedrichstraße 123, Berlin 10115 · VAT DE123456789

- Line 1: UX research & wireframes — 40 hours × €75/hour = €3,000.00

- Line 2: Design system tokens — 20 hours × €75/hour = €1,500.00

- Subtotal: €4,500.00

- VAT (0% — reverse charge, intra-EU B2B): €0.00

- Total: €4,500.00

- Note: “Reverse charge applies per Council Directive 2006/112/EC, Article 196. VAT to be accounted for by the recipient.”

- Pay to: Swedbank LV · IBAN LV12HABA0000000000123 · BIC HABALV22 · Studio Vesper SIA

That's a complete, legally-clean cross-border invoice. The German client's AP team can process it without sending a single follow-up question. Here it is as a finished PDF:

Common mistakes that delay payment

- Missing PO number. If the client gave you a purchase order, quote it on the invoice. Without it, the invoice may sit in a “needs matching” queue for weeks.

- Inconsistent business name. The name on the invoice must exactly match the name on the contract and on your bank account. Even small mismatches (“Ltd” vs “Limited”) can trigger AP holds.

- Vague descriptions. “Consulting services” reads like a placeholder. “Q1 2026 onboarding flow — 40 hours” is auditable.

- No payment terms. Always include “Payment due 14 days from invoice date” (or whatever you agreed). Without it, the client's default terms apply — and those can be 60+ days.

- Wrong currency for the client. If you agreed EUR, don't send a USD invoice and ask them to figure out the conversion. Match the contract.

Even a flawless invoice sometimes goes unpaid. When it does, don't let it drift — here's how to chase an unpaid invoice politely with a calm reminder sequence.

EU-specific essentials

If you're VAT-registered and selling to another EU business that's also VAT-registered, you usually don't charge VAT — you apply reverse charge. The buyer accounts for VAT in their own country. To do this correctly:

- Show 0% VAT on the line items.

- Include both VAT numbers — yours and the client's.

- Add a note like “Reverse charge — Article 196 of Directive 2006/112/EC.”

- Report the sale in your EC Sales List (called Recapitulative Statement in some countries) the next quarter.

If you're selling to a private individual in another EU country (B2C), the rules are different — see the OSS scheme. For non-EU clients, VAT is typically zero-rated, but you'll still want a clear note explaining why.

FAQ

Do I need a VAT number to invoice as a freelancer?

Not always. In most EU countries, registration is required only above a turnover threshold (€40,000 in Latvia, €22,000 in Germany, €85,000 in France for B2C services in 2026, etc.). Below it, you can invoice without VAT — but you also can't reclaim input VAT on business expenses. Voluntary registration is often worth it once you have steady B2B clients.

What if my client is in a different EU country?

If they're VAT-registered, apply reverse charge (0% VAT, both VAT numbers on the invoice, note quoting Article 196). If they're a private individual, you charge your local VAT — or theirs, if you're past the EU-wide €10,000 distance sales threshold, via OSS.

Can I invoice in a currency other than EUR?

Yes. You can invoice in any currency you and the client agree on. For tax reporting, you'll usually need to convert to your local currency using the official rate on the invoice date — most tax authorities accept the European Central Bank reference rate.

What to read next

- What to Include on an Invoice: The Complete Checklist

What to put on an invoice: a copy-paste checklist of every field a professional invoice needs — EU-specific extras and the optional bits that quietly accelerate payment.

- How to Chase Unpaid Invoices Politely: Templates + Late-Payment Interest

Chase unpaid invoices and get paid — a calm five-step sequence with copy-paste reminder email templates, when to send each one, and the late-payment interest you're owed.