Reverse Charge: Cross-Border EU B2B VAT Explained

Why you charge 0% VAT on services to EU business clients, the Article 44 and 196 rules, VIES checks, and the exact invoice wording to use in 2026.

A client in another EU country hires you, and their accountant insists you must not add VAT. Your instinct says that's wrong — surely tax is always due? It isn't, and the rule that explains it is called the reverse charge. Here is exactly when it applies, when it doesn't, and the wording your invoice needs.

This builds on the basics in our plain-English guide to VAT for EU freelancers.

What is the reverse charge?

The reverse charge is a mechanism where, for cross-border B2B services within the EU, you (the supplier) charge 0% VAT and your business customer accounts for the VAT in their own country instead. Two articles of the VAT Directive (2006/112/EC) do the work:

- Article 44 — the general place-of-supply rule for B2B services: the place of taxation is where the customer is established, not where you are.

- Article 196 — because the supply is taxed in the customer's country and you are not established there, the customer becomes the person liable to pay the VAT.

For a fully taxable customer the net cash effect is zero: they declare the VAT as output VAT and deduct the same amount as input VAT on the same return. The obligation is real, but the money washes out.

When does it apply — and when does it not?

It applies to services supplied to a VAT-registered business in another EU country; it does not apply to consumers, to same-country sales, or (in the same way) to goods.

| Situation | What you do |

|---|---|

| Service to a business in another EU country | Charge 0%, apply the reverse charge |

| Service to a private consumer (B2C) in another EU country | Reverse charge does not apply — see the B2C and OSS rules |

| Service to a client in your own country | Charge your domestic VAT as normal |

| Goods sold to a business in another EU country | Different regime: intra-Community supply (Art. 138) / acquisition |

Goods are not services. A cross-border sale of goods to an EU business is an intra-Community supply exempt under Article 138, matched by an intra-Community acquisition by the buyer — with its own invoice wording (e.g. “Exempt intra-Community supply — Article 138 of Directive 2006/112/EC”). Don't mix up the two.

Step 1: validate your customer in VIES

Before you zero-rate anything, confirm your customer's EU VAT number in the European Commission's VIES system and keep the proof. VIES (VAT Information Exchange System) is the EU's free online tool for checking that a VAT number is valid. If the number is invalid, you should treat the customer as a non-business (B2C) and the reverse charge protection may not apply — potentially leaving you liable for the VAT you didn't charge.

Step 2: use the right invoice wording

Article 226(11a) of the VAT Directive requires the words “Reverse charge” on the invoice; citing Article 196 is widely recommended best practice but is not strictly mandated by the Directive itself. A safe, universally accepted form is:

Reverse charge — VAT to be accounted for by the recipient under Article 196 of Council Directive 2006/112/EC

Your invoice must also show both your own VAT number and the customer's VAT number. Many countries also accept a local-language equivalent (German Steuerschuldnerschaft des Leistungsempfängers, French Autoliquidation, Dutch btw verlegd).

Step 3: report it on your EC Sales List

Cross-border B2B services under the reverse charge must be reported on a recapitulative statement (the “EC Sales List”), required by Articles 262–264 of the VAT Directive. This is how tax authorities cross-match that the customer in the other country actually declared the VAT. The statement is called the Zusammenfassende Meldung (ZM) in Germany and the DES in France.

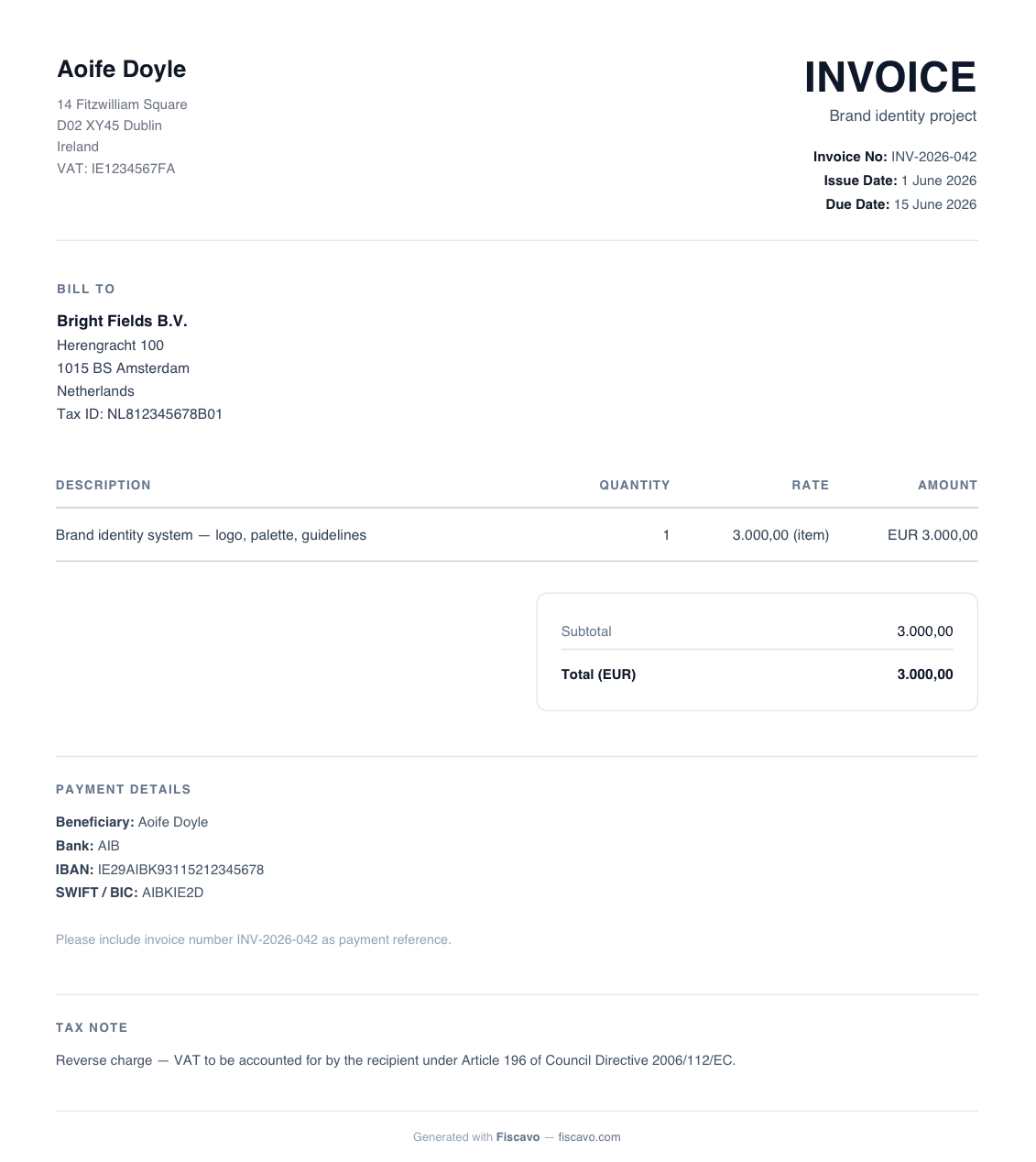

Worked example

You are a VAT-registered designer in Ireland. You bill a VAT-registered agency in the Netherlands €3,000 for a brand project. You validate their Dutch VAT number in VIES (and save the result). Your invoice shows €3,000, VAT 0%, both VAT numbers, and the Article 196 wording. The Dutch agency self-accounts for Dutch VAT at 21% (€630 output and €630 input — net zero). You include the sale on your Irish recapitulative statement. No Irish VAT, no Dutch registration needed.

Frequently asked questions

What is the VAT reverse charge?

The reverse charge is a mechanism where, for cross-border B2B services within the EU, the supplier does not charge VAT and the business customer accounts for it instead in their own country. Under Article 44 of the VAT Directive the place of supply is the customer's country, and under Article 196 the customer becomes liable for the VAT.

What wording must a reverse-charge invoice include?

Article 226(11a) of the VAT Directive requires the words “Reverse charge” on the invoice. Citing the legal basis is best practice though not strictly mandatory; a widely accepted form is: “Reverse charge — VAT to be accounted for by the recipient under Article 196 of Council Directive 2006/112/EC.” You must also show both your VAT number and the customer's VAT number.

Do I need to check my client's VAT number?

Yes. Before applying the reverse charge you should validate the customer's EU VAT number in the European Commission's VIES system and keep proof of the check. If you apply the reverse charge to an invalid number, the protection of the mechanism may not apply and you could be left liable for the VAT.

Does the reverse charge apply to consumers or domestic sales?

No. The intra-EU reverse charge for services applies only to business customers (taxable persons) in another EU country. It does not apply to B2C sales to private consumers, and a sale to a client in your own country normally carries your domestic VAT in the usual way.

What to read next

- What Is VAT? A Plain-English Guide for EU Freelancers

What VAT is, how output and input VAT work, and what changes when you register — explained for EU freelancers and small businesses in 2026.

- VAT on B2C Sales, OSS and Exports Outside the EU

The €10,000 OSS threshold, when to charge customer-country VAT, the One-Stop-Shop, zero-rated exports and services to non-EU clients — for 2026.